The price of the products is the whole of the actual cost to produce complete a unit of product, including the cost of materials, labor, and production overhead. This is the index helps determine the price of capital, construction, sale price, not the sale price market. Determine the right price to help businesses control costs as well as decision-making executive accurate.

Many enterprises still face difficulties due to cost classification has a standard allocation of indirect cost was estimated and choose the method of price calculation is not appropriate. This price deviations from the fact, entail risks in the selling price, performance evaluation as well as financial management.

So, businesses need to understand the true nature price, the cost components to choose methods appropriate to control costs and maximize profits. The article below Lac Viet will the same business learn as well as clarify the concept of price of the product, classifications and methods work in practice management.

1. Product price is what?

1.1 product Price accounting – finance

The product price is the total actual cost businesses have to spend to produce a unit of product in a period, not the selling price, which is the cost for the product is formed and ready to put on the market. In accounting, the price is set from the expenses directly to the production such as raw materials, direct, direct labour and production costs, general, reflect the full extent of the shrinkage of resources that the business must take to create the product.

Differentiate prices & product sale price

The price, the sale price products are two concepts closely related but serve the target completely different in governance and business accounting.

| Criteria | Price of the product | Sale price product |

| Nature | The cost to create the product | Price business transactions |

| Purpose | Base price of capital, profit and cost control | Service sales target, the optimal revenue |

| Base form | Based on the actual cost incurred in the production | Based on cost, profit margin and market factors |

| Impact factor | Production processes, productivity, cost control | Competition, customer needs, business strategy |

| Properties | Bearing the internal service management | Iconic market, catering business |

Note: If pricing is missing or wrong, the business can determine the selling price wrong (too low or too high), leading to risk of loss, loss конкурент force or misjudged business performance.

The role of the product price in financial reporting & internal management

the price of product is only goal of accounting is important, at the same time as data platform, service management and decision making in business. In particular, the price has the following roles:

- Base notes cost of goods sold (COGS): COGS reflect the actual cost of products sold; determine the right price to help reflect the gross profit.

- Impact on financial performance & obligations tax: Price directly affects the profit margin, profits taxable. Wrong price wrong evaluate the effectiveness as well as potential tax risks.

- Provide data for cost management & decision-making: the Price of help track fluctuations in cost, performance evaluation, each stage as a basis for improvement and investment.

1.2 why businesses need special care to product price?

In financial management – accounting price of the product is the administration tool to help businesses understand the true cost, effective control and direction of business. Therefore, businesses need special attention to price because of the following reasons:

- Price is base building strategy selling prices right: Grasp the exact price helps determine the minimum selling price with interest, the amplitude of the price matching. The price lower than the price of long-term causes a loss, also the high prices when the cost has not optimally reduce competitiveness. Control good price allows the construction of price policies, discounting and promotional logical that still ensuring profit.

- Price is a measure of production efficiency – business: compare prices over time, between the lines, or menu item help detect points of congestion costs, to assess the effective use of resources, from which leaders have timely basis optimal processes, restructuring or technology investment.

- Price is platform to control cost & optimal profit: analysis component prices to help identify the cost of not creating value, monitor to detect anomalies, from which business can reduce the cost reasonably, improve profit margins, as well as enhance competitiveness.

Price so not only technical indicators which are pillars of the system of cost management. standardized tracking methods, cost analysis is the foundation for the decision management and long-term strategy of the business.

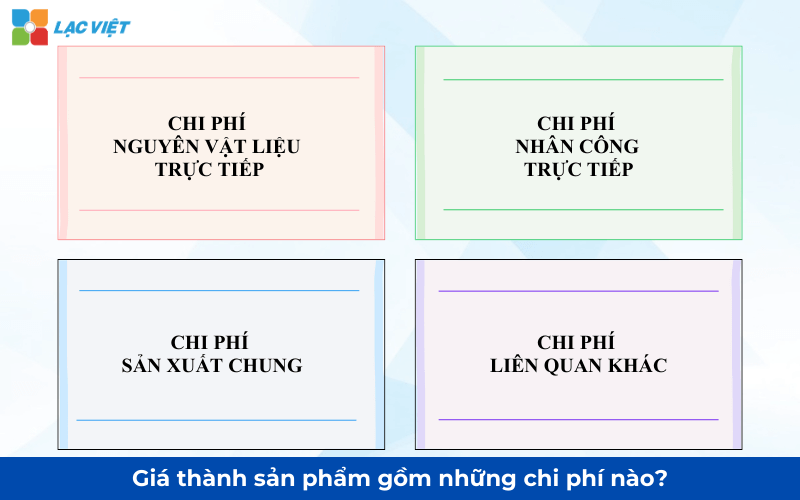

2. The product price includes cost?

Businesses often incorrect price due to the identification as well as sorting costs not true. Especially confusion between the cost price, cost states. According to the current accounting year, the price of the product, including the three main costs and some costs directly related.

2.1. The cost of raw materials directly

The cost of direct material is the total value of materials used directly to create the product, including:

- Main materials: the material constituting the bulk texture of the product, for example in furniture manufacturing is raw wood.

- Extra materials: raw materials, support finishing products such as paints, glues, accessories...

- Semi-finished products purchased outside: the parts have been machined part and put in the process of finishing products.

In structure, the price of the product, the cost of raw materials directly often accounted for a large proportion (usually 30%-70% of the total production costs). Direct influence on business results, so cost control is the key element to the product prices, improve profit margins.

Illustrative example: In a manufacturing business furniture

- Wood raw materials determine the structure and quality products

- Paint, glue, metal fittings material is mature, but indispensable in the process of finishing

All these amounts are set at the cost of direct material of each product or order.

2.2. Costs directly

Costs directly cover the entire costs related to workers directly involved in production, in particular:

- Wages over time or according to the product

- Allowances bring food quality

- Deductions from wages as social insurance, health insurance, unemployment insurance in accordance

Only direct labor created new product is calculated into the cost of direct labour. Labor management and indirectly to be accounted for into the cost of joint production or cost management.

The influence of the productivity of labor to the price of the product. In fact, the same salary, but:

- If low productivity → cost per unit of product increase

- If high productivity → cost allocation on each product reduction

Therefore, the price of the product reflects not only wages, but also reflects effective organization of production, skilled labor and the level of standardization processes.

2.3. The cost of production in common

Production overhead is the indirect cost, but necessary to the production activities take place, including:

- Depreciation machinery, equipment, buildings

- The cost of electricity, water, fuel production service

- Cost of repairs, maintenance, machinery

- Salary costs related to staff management workshop

This is the cost hard to follow prone to allocate wrong, especially with businesses that have multiple lines or more types of products.

These costs are often overlooked when calculating the price in business:

- The cost of minor repairs arising regular

- The cost for tools to allocate more states

- The cost to hire technical services, maintenance, safety production

The omission of this clause, causing the price of products is lower than the actual leads to false when profitability analysis.

2.4. Other costs are related to the price of the products

In addition to the three main costs, a number of other costs can still be calculated into the price if directly related to creating the products, for example:

- Machining cost outsourced by stage

- Cost of inspection, test and evaluate the quality of products before enter warehouse

These amounts generally arise unevenly, but if not, be followed are prone to “drift” to cost states, distort prices.

Cost segregation charged to prices & costs not charged to the business need to distinguish:

- Cost calculated in the price: only include the costs tied directly to the production

- Costs not included in the price: cost of sales, cost management, business, finance charges – is accounted for by the states and not allocated to cost of production

3. Product prices how to calculate?

In fact, the price of products is the basis for decisions about price, production planning and cost control. If the method does not fit data, whether true books still no support for effective management.

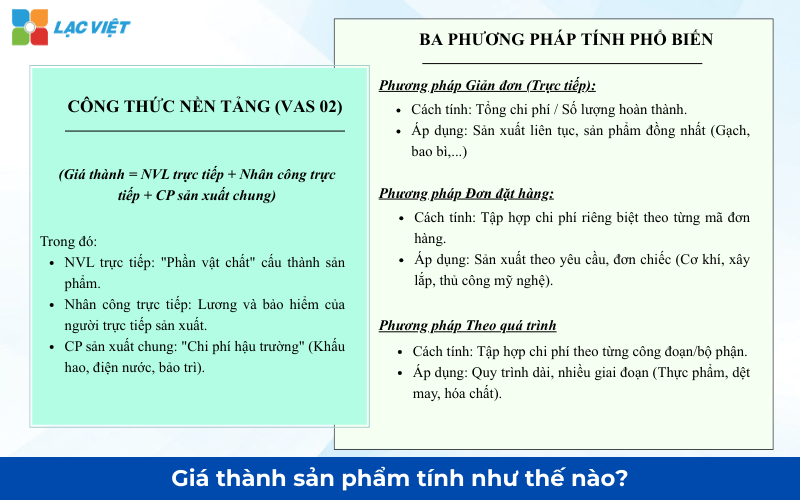

3.1. Formula for calculating the price of the basic product

According to the principle of accounting for the price of the product cost is determined by the formula:

(Product cost = Cost of direct material + Cost of direct labour + manufacturing Costs general)

In which:

- The cost of direct material: the entire cost for the type of supplies used directly to create products. Can understand simple this is “the visible physical” structure of the product.

- Cost, direct labour: Is the cost paid to the employee directly made products, including the salaries, allowances and deductions from wages as prescribed.

- The cost of production in common: That the indirect costs, but indispensable to production, such as depreciation, machinery, electricity, water workshop, maintenance costs, production management. Can understand this is the “cost the scenes” to help produce stable operation.

This is a recipe platform which is used uniformly in the system accounting standards and accounting regime prevailing in Vietnam, especially is specified in the accounting Standards of Vietnam 02 – inventory.

3.2 The method of calculating the price of popular products today

The method of calculating the price of simple

Method simple is the whole set of production costs incurred in the period for a product type, then allocate all costs this for the number of the finished product. Method in accordance with the business are the production process simple, self-contained, short cycle and homogeneous product or have the cost difference is not significant between the product lines.

When business should apply

- Business process, continuous production closed (for example: concrete, brick, packaging, insulation sheet).

- Products less volatility in terms of categories or do not need to track expenses detailed in the paragraph.

- Cost allocation is considered to be evenly over the entire finished product.

This method helps simplify the recording costs, in accordance with medium enterprise/ small unorganized accounted for by the stage; however, if the product variety or indirect costs accounted for a large proportion, accuracy in cost analysis, as well as the selling price may be restricted.

Illustrative example: A business manufacturing packaging for 6 months total cost of production is 1.200.000.000 and complete 20,000 products, there is no unfinished products end – to-end states.

The price of units is determined as follows:

Price unit = 1.200.000.000 / 20.000 = 60.000/products.

This result helps business basis to determine the selling price calculate profit compared with the previous period to evaluate the effectiveness of cost control.

The method of calculating the cost of orders

This method determines the cost of production on each specific orders, considered each order as a “cost object” private and set direct cost on that order. Production overhead is allocated by reasonable grounds (such as hours of work, hours of machine).

This is the method in accordance with the business produced according to customer requirements or according to each project in retail, not mass-produced uniformity.

Strengths in management

- Cost analysis details by each order helps to control input costs, compared to the cost of the plan.

- Optimize the selling price for each contract, improving the profit margin.

- More clear when customer requires cost transparency.

This method is applied for manufacturing enterprises as simple as machinery design, separate crafts or construction; the cost is set and allocated separately for each contract to determine the price.

The method of calculating the cost of the production process

This method aggregates expenses according to each stage of production or parts, then calculate the price of the average for the finished product in the states. It business suit mass production process, many stages.

Strengths in management

- Reflect the cost according to each stage, help analyze efficient operation each workshop, manufacturing organization.

- Business support, construction norms, cost control, more effective in mass production.

When should I apply this method:

- Business production, food processing, textiles, chemicals, cement...

- The product line has many stages, difficult to split the cost for each unit of product individually.

This method of creating paintings cost details on each step production, help leadership have data for resource allocation, optimal production capacity and improve the quality of the forecast price of the plan..

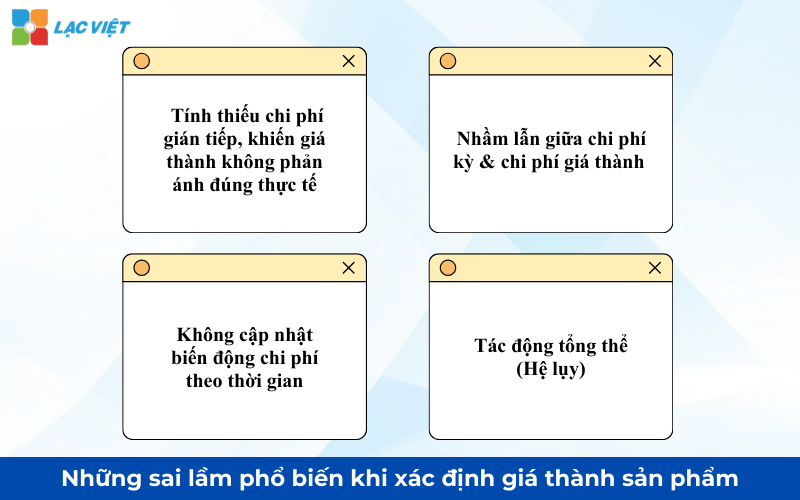

4. Common mistakes when determining the price of products in the enterprise

In practical advice, much deviation about the price does not come from lack of that recipe from the identification, handling costs, not true essence. If prolonged, the business can fall into a state of increased revenue, but profit does not increase, even without identifying the cause.

4.1. Teen indirect costs, making the price not reflect the actual

A very common mistake is business only focus on the cost of materials and labor, while the cost of production would be set sketchy or allocate an estimate.

The account is often overlooked or underestimated, including:

- Depreciation of machinery and equipment production

- The cost of maintenance, repair arises frequently

- Water, electricity, fuel used for the workshop

- Cost management production

When indirect costs are not allocated the full price of the product is “beautiful” than it actually is, leading to the sale price too low. Businesses can still make a sale, but real profit is not commensurate with the effort as well as resources spent.

4.2. Confusion between the cost of states & the cost price

Many businesses, especially the small & medium business, still confused between:

- The cost calculator on the product price (cost attached directly to the production process)

- Costs such as cost of sales, cost management, business

Putting the costs not directly related to production on price will make the price of being team-up not required, to make it difficult to compare between the products, the states, or other orders.

Conversely, if “push” production costs out to cost states, price of the product is lower than reality, distort reviews production efficiency.

This mistake not only affect the reported internal management, but also can pose a risk when profitability analysis, construction budget as well as business decisions long-term.

4.3. No updates fluctuations in cost over time

In the context of the price of raw materials, wages and input costs constantly fluctuating, many businesses are still:

- Use cost norms in long time

- Don't revise the price when production conditions change

This makes product prices no longer reflect the reality at the present time. Meanwhile, leaders still make decisions based on data, “obsolete”, which leads to deviations in the selling price, production planning as well as control the profits.

With respect to the organizations and enterprises are to find out information about the price of the product, this is a big risk if the system management accounting is not flexible enough to update as well as analysis of fluctuations in costs in real time.

4.4. The overall impact of the mistake on the

If the mistake is not remedied promptly, the business will face:

- the price of products reliable

- Hard to control, profit margin realistic

- Business decisions based on inaccurate data

In the long term, this is the cause deterioration of competitiveness, especially in the environment of market volatility.

5. Accounting software Accnet ERP support cost effective product for business

AccNet ERP is the solution designed in accordance with the characteristics operating standards, the Vietnamese accounting. Serve manufacturing enterprise in controlling the optimal cost and decision support executive.

Instead of just stopping in the recorded data, AccNet ERP helps businesses:

- Set cost automatically according to each object price: AccNet ERP data link purchasing, warehouse, manufacturing, accounting to automatically record the cost according to the product, stage, orders or lines, helps reduce manual action, limit errors, as well as ensure data rates of consistency.

- Allocation of cost, accuracy, transparency: The software allows setting the allocated according to the actual production (production, hours of machine consumption,...), help to allocate indirect cost police more practical as well as improve the quality of reporting prices.

- Analysis of fluctuations in price over time & objects: AccNet ERP allows comparing the price of the products, orders or chains to determine the cause fluctuations in costs to support the timely adjustment.

- Support governance decisions based on data: cost Data is standardized analysis focus on helping leaders decisions more precise in control costs and maximize profits.

INTEGRATED AI ACCELERATION CONVERTER OF ACCOUNTING

AI in AccNet ERP't just stop at automate data entry, but also:

- Identification & classification certificate from smart: AI scan, read & sort invoice, voucher, receipt, limit errors due to input manually.

- Financial forecasting & budget: the system uses algorithms machine learning to forecast cost, revenue, business support decision fast.

- Warning risk accounting: AI to detect abnormalities in the book, from which timely warning of false or fraud risks.

- Reports assistant smart: AI suggested report template, automatic data aggregation support, leadership, financial analysis instant.

BUSINESS IS WHAT WHEN IMPLEMENTING ACCOUNTING SOFTWARE LAC VIET?

- Experience more than 30 years develop software solutions business management in Vietnam.

- Ecosystem of comprehensive: AccNet ERP easily connect with other solutions of Lac Viet (HRM, Workflow, Portal...).

- Advanced technology: Integrated AI support, cloud & on-premise flexible.

- Services dedicated support: A team of knowledgeable professionals with accounting – finance in Vietnam, companion throughout the deployment.

- Trust from thousands of customers in many areas: finance, banking, manufacturing, trade, services.

The price of product is only the core goal reflects the quality cost management in the operational efficiency of the business. Determining the correct, timely price help business valuation reasonable control, profitability, and enhance the competitiveness. In the context of cost fluctuations, management price should be approached in the direction system in data encryption, fastened with out operating decisions. Mastered price as a condition for business sustainable development on the platform is the most effective substance.