Hạch toán hàng khuyến mại thường không ghi nhận doanh thu mà được tính vào chi phí bán hàng (TK 641) hoặc giá vốn hàng bán (TK 632). Khi xuất hàng khuyến mại, kế toán ghi Nợ các tài khoản chi phí và Có TK 155, 156. Trường hợp chương trình khuyến mại đăng ký hợp lệ, giá tính thuế GTGT bằng 0. Nếu không đăng ký, doanh nghiệp phải xuất hóa đơn và tính thuế GTGT đầu ra vào chi phí hoặc giá vốn.

However, in fact, many businesses still have difficulty handling situations promotion as diverse as the gift of not collecting money, sales with promotional conditional or promotions are not registered with Department of Trade and Industry. Identifying the wrong nature, business or accounting is not properly can lead to false charges, false VAT and increase in risk when settlement tax inspectors.

In this article, along Lac Viet understand the concept of promotional items, classifications, principles of accounting according to the circular 133 & circular 200, at the same time guide how to record accounting at sell-side and buy-side with illustrative examples practical help in accounting applied easily in the implementation process.

1. Overview of recorded business promotional items

1.1. Accounting promotional item, what is?

Accounted for promotional goods is recorded and processed in accounting for the goods and services businesses use to promotion to customers to promote sales as well as enhance the experience. In essence, promotional items is the cost of sales promotion, not revenue from operations sale of products. Therefore, the accountant should clearly distinguish with sales transactions often to record the exact cost, revenue, and tax obligations.

The role of accounting in business operations:

- Support promoting sales of short-term: The promotion, as gift, sell, preferential price, help to stimulate purchasing decisions, particularly in the peak period.

- Increase brand awareness: promotional Items, especially the products are used regularly, help brands appear constantly in the process of consumption of the customer.

- Deployment tool sales strategy according to each stage: properly account for promotional items help business expense tracker promotion for goals such as new product launches, in global or handling inventory.

Professional services, promotional goods, not only to recognize the cost, but also the basis for assessing program effectiveness, sales, cost control and compliance with tax regulations, in particular with the case of promotional goods not registered with department of trade and industry.

1.2. The type of sales promotion frequently in accounting

Classification of the right promotional items is an important step in accounting, by every form of promotion will last way recorded cost, revenue, and different VAT. If the wrong type, business accounting the wrong accounts, wrong tax or risk when the settlement.

The form of popular promotional in accounting include:

- Hàng khuyến mại không thu tiền: Doanh nghiệp tặng hàng cho khách mà không gắn với điều kiện mua cụ thể, như quà tri ân hoặc vật phẩm quảng bá. Trường hợp này thường được hạch toán vào chi phí bán hàng, nếu chương trình đăng ký hợp lệ, không phải tính thuế GTGT đầu ra.

- Hàng khuyến mại có điều kiện (bán kèm): Hàng khuyến mại chỉ phát sinh khi có giao dịch bán hàng, ví dụ “mua 10 tặng 1”. Kế toán cần phân bổ giá trị hợp lý giữa hàng bán cũng như hàng khuyến mại để phản ánh đúng doanh thu, giá vốn và lợi nhuận.

- Giảm giá hàng bán: Là hình thức điều chỉnh giá bán, không phải tặng hàng. Kế toán cần phân biệt rõ với hàng khuyến mại để hạch toán đúng tài khoản giảm trừ doanh thu theo quy định.

- Trade discount: Áp dụng cho khách hàng mua số lượng lớn hoặc đạt doanh số cam kết. Khoản chiết khấu này làm giảm doanh thu và cần được theo dõi riêng để đánh giá hiệu quả chính sách bán hàng.

- Phiếu quà tặng, vật mẫu: Thường dùng để giới thiệu sản phẩm mới hoặc kích thích dùng thử. Dù giá trị từng đơn vị nhỏ, kế toán vẫn cần theo dõi riêng để kiểm soát chi phí nhằm chứng minh tính hợp lệ khi quyết toán thuế.

From the perspective of accounting, the classification of the right promotional item is the platform to record the exact cost, regulatory compliance, taxes, and limited risk.

2. Accounting principle promotional items

Promotional items are just related to cost, just directly affect VAT and business results. So, master the principles of accounting will help the business avoid errors, as well as financial control efficiency.

2.1. Accounting principles generally apply to promotional items.

- Promotional item not as active sales revenue-generating independent, which is the cost of servicing sales promotion.

- In the majority of cases, accountants do not recognize revenue for the promotional item, which is recorded in cost of sales or cost of goods sold.

- With the cases accounted for promotional goods not collect money, businesses should have sufficient records to prove promotions valid.

- If the program is not registered with Department of Trade and Industry, business promotion can be considered gifts to charge output VAT as sales usually increase the cost and tax risks.

2.2. Principles of cost allocation promotion according to TT133 & TT200

- Promotional costs must be recorded on the revenue is earned and the right audience to bear the costs.

- With regard to the sales program with promotion, accountants need to allocate the fair value between the sale and promotional items.

- This principle is particularly important in recorded promotional goods, conditionally, to reflect revenue, price, capital and profit.

- Compliance with accounting promotional goods, according to Circular 200 help accounting data consistency, ease of exposition, the tax settlement.

2.3. Impact on financial statements & business results

- Promotional goods, directly affecting cost of sales, profits, and tax obligations of the business.

- Recorded may falsely falsifying business results affect the financial criteria decision management.

- According to the General department of Taxation, the cost of sales and cost of promotion is to group the cost is usually scrutinize when inspection due to errors on the tax

- Properly accounted help business financial transparency, reduce risk arrears improve the quality of information service management.

3. Accounting maths promotional items at the seller – business organization promotion

On the side of the seller, the accountant should clearly define the nature deals (registered or not, conditional or not) to choose the way of accounting and handle proper VAT.

3.1. Cargo payment for promotion does not collect the money with no conditions (Have a valid registration)

This is the most common case in practice, often applied with gifts, every trial, every brand promotion.

Accounting principles:

- Promotional goods, non-revenue generating.

- Value promotional items are recorded as cost of sales.

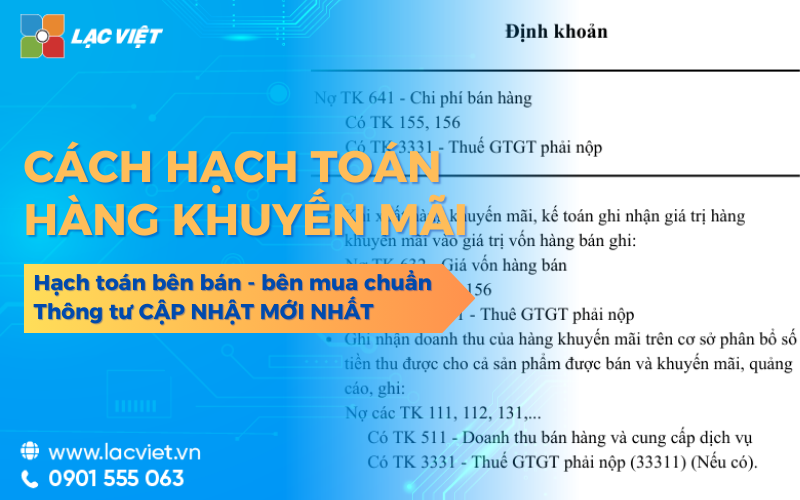

How accounting as export promotion: accounting value of goods into cost of sales

- Debt TK 641 – Cost of sales (TT200)

- Debt TK 6421 – Cost of sales (TT133)

- Have TK 155, 156 – inventory

Accounting VAT (if the program is valid subscription):

- TAXABLE price equal to 0.

- Accounting does not record output VAT for the promotional item.

Properly accounted help business recorded a reasonable cost, do not arise VAT is not necessary and reduce the risk of settlement.

3.2. Accounting promotional goods, there are conditions attached (Method of allocation of revenue)

This case occurs when the promotion is only awarded if the customer purchases the product itself, for example “buy 10 get 1 free”, “buy product package may gift with”.

Accounting principles:

- Revenue is recorded according to the total amount the customer actually paid.

- Value promotional items are allocated to the cost price or cost.

Revenue recognition & VAT:

- Debt TK 111, 112, 131

- Have TK 511 – sales revenue, service provider

- Have TK 3331 – VAT outputs payable

Recorded the price of capital:

- Debt TK 632 – cost of goods sold

- Have TK 155, 156

Properly accounted promotional items conditionally help to accurately reflect the revenues and profits and avoid the status of “team” revenue or false profit margin.

3.3. Accounted for promotional goods not registered with department of trade and industry (considered a donation)

This is the situation high risk of tax that many businesses encounter.

Accounting principles:

- Promotional items no registration is considered to be goods, and gifts.

- Business must charge VAT output as sales usually.

Recorded cost or price of capital:

- Debt TK 641 / TK 6421

- Have TK 155, 156

Record output VAT (under the price):

- Debt TK 641, 6421

- Have TK 3331 – VAT payable

Identify early cases accounted for promotional goods not registered with Department of Trade and Industry to help businesses proactively handle taxes, avoid arrears and late payment penalties.

3.4. Accounting discount wholesale/trade Discount

This form of price adjustment, not awarded restaurant.

Circular 200:

- Debt TK 521 – The sales deductions

- Debt TK 3331

- Have TK 111, 112, 131

According to circular 133:

- Debt TK 511

- Debt TK 3331

- Have TK 111, 112, 131

Properly accounted help businesses determine the net revenue accurately, the assessment of effective sales policy.

4. Accounting maths promotional items at buy-side – business to receive promotional goods,

On the side of the buyer, the accountant should clearly distinguish promotional goods received have to pay or not to recognise the true nature.

4.1. Get promotional items not paid (Goods, supplies, patterns)

This is the case, the business receiving goods from suppliers, often in the form of samples, gifts with contract or sales support. In essence, the enterprise does not arise payment obligations, but still get the economic benefits from this goods.

Accounting principles:

- The donation is recorded as the property of the business.

- Value of goods shall be determined according to the fair value or the estimated price at the time of receipt.

How accounting:

- Debt TK 152, 153, 156 (according to fair value/estimated)

- Have TK 711 – other income

Properly accounted help businesses fully reflect the inventory record to get the right income arises, avoid the omission of assets and ensure the transparency of financial reporting.

4.2. Purchase with promotional products (Package)

In this case, the business of purchase to receive more promotional items comes, but the total payment value already includes the promotion. This is a situation often encountered in practice a large quantity purchases or purchases under the program of preferential treatment of suppliers.

Accounting principles:

- The total value of payments should be allocated logical for each type of goods received.

- Input VAT is deducted according to the valid invoice.

How accounting:

- Debt TK 156 (according to the values already allocated)

- Debt TK 133 – VAT deductible

- Have TK 111, 112, 331 – the Total value of payments

The allocation of the right to help businesses determine the exact cost of goods, inventory, avoid or reduce the cost not true fact, from that properly reflect the profit in the period.

4.3. Enjoy the discount trade discount sale

Trade discount or price reduction seller's price adjustment that business is entitled to when buying goods in bulk or qualify sales under the agreement.

Accounting principles:

- Account the discount or the discount reduces the value of the purchase.

- Input VAT corresponding also to adjust up.

How accounting:

- Debt TK 111, 112, 331

- Have TK 152, 156

- Have TK 133

Properly account for the discount discounts help the business recorded input costs, accurate analysis service effective purchasing and control profit.

5. For example, accounted for promotional goods between the seller and the buyer

To the organizations and enterprises are to find out information about top promotional easily visualize, here is a real example frequently.

Situation: company A (the seller) to deploy promotions have duly registered with Department of Trade and Industry: “Buy 10 product X, get 1 product X”.

- Sale price before tax of 1 product X: 1,000,000

- VAT: 10%

- Customer is company B (buyer)

- Total items: 11 product, customer, payment of 10 products

In the seller – company A

Nature business: Goods with is the promotion conditions, arising in sales activity and have valid registration.

How accounting:

- When exporting, collect money:

- Debt TK 111, 112, 131: 11.000.000

- Have TK 511: 10.000.000

- Have TK 3331: 1.000.000

- Recorded the price of capital for the entire 11 products warehouse:

- Debt TK 632

- Have TK 155, 156

The allocation of revenue in the form of this help business proper recognition of revenue, don't overlook the cost of compliance with accounting principle promotional item, circular 200.

In the buyer – company B

Nature business: Business purchase in the packaging and enjoy a promotional attached.

How accounting:

- Recorded inventory by price allocation:

- Debt TK 156: 10.000.000

- Debt TK 133: 1.000.000

- Have TK 111, 112, 331: 11.000.000

The allocation of the right to help the buyer determine the cost of reasonable, avoid recorded false charges, especially important when analyzing business performance.

6. A number of issues should be noted when performing accounting

In actual deployment, business accounting often encounter some errors common following:

- Confused between promotional goods, registered and not registered: may lead to accounting sai VAT. If promotional items are not yet registered with regulatory authorities, the tax may be considered the items donated and requires the calculation of VAT output as sales usually.

- Accounting sai VAT: Occurs when no invoice or invoice, but do not adjust the tax properly with essence top promotion, though not collect money or conditional. This error is at risk of arrears and penalties when the tax check.

- Do not separately track promotional costs according to each program: Pooled cost makes business difficult to assess the effectiveness each sales campaign, at the same time reduces the ability to control the budget for marketing.

- Teen records & vouchers valid: The evidence from as decided promotions, notification register, program regulations, the invoice store is an important base to protect expenses when tax settlement. The lack of this profile, promotional costs are at risk for type.

Accounting right from the beginning not only help businesses comply with legal regulations, but also improve the quality of financial reporting, as well as the ability to control the cost of sales.

7. Management accounting, optimized business with accounting software Accnet ERP

Trong thực tế, thực hiện nghiệp vụ hàng khuyến mại theo Thông tư 133 & Thông tư 200 dễ phát sinh sai sót do nhiều tình huống khác nhau yêu cầu xử lý thuế phức tạp. Accnet ERP là phần mềm kế toán cho doanh nghiệp lớn giúp các doanh nghiệp Việt chuẩn hóa và tự động hóa toàn bộ quy trình này.

- Automatic accounting nature business: Recorded exactly the case, promotional goods, do not collect money, conditional or not yet registered with Department of Trade and Industry ensure the correct use of accounts and tax reasonable.

- Track promotional costs according to each program: Costs are detailed management under the program, contract, or clients, helping businesses evaluate the effectiveness of sales promotion more clearly.

- Control VAT & risk settlement: System management support bill promotion, specify the correct case, the tax price is equal to 0 or to charge output VAT, limit your risk when the tax inspection.

- Data link sales – inventory – accounting: data export warehouse, the price of capital and the cost of promotion is synchronized, helping financial statements reflect true business results.

- Compliance with accounting standards: keep abreast of circular 133 & circular 200, help business accounting regulations.

INTEGRATED AI ACCELERATION CONVERTER OF ACCOUNTING

AI in AccNet ERP't just stop at automate data entry, but also:

- Identification & classification certificate from smart: AI scan, read & sort invoice, voucher, receipt, limit errors due to input manually.

- Financial forecasting & budget: the system uses algorithms machine learning to forecast cost, revenue, business support decision fast.

- Warning risk accounting: AI to detect abnormalities in the book, from which timely warning of false or fraud risks.

- Reports assistant smart: AI suggested report template, automatic data aggregation support, leadership, financial analysis instant.

BUSINESS IS WHAT WHEN IMPLEMENTING ACCOUNTING SOFTWARE LAC VIET?

- Experience more than 30 years develop software solutions business management in Vietnam.

- Ecosystem of comprehensive: AccNet ERP easily connect with other solutions of Lac Viet (HRM, Workflow, Portal...).

- Advanced technology: Integrated AI support, cloud & on-premise flexible.

- Services dedicated support: A team of knowledgeable professionals with accounting – finance in Vietnam, companion throughout the deployment.

- Trust from thousands of customers in many areas: finance, banking, manufacturing, trade, services.

>>> Doanh nghiệp quy mô nhỏ có thể tham khảo phần mềm kế toán doanh nghiệp vừa và nhỏ để quản trị tối ưu chi phí nhất

Accounting promotional item, circular 133 & 200 potential risks if the business do not understand the true nature. Categorised properly recorded reasonable cost under the VAT help control the cost of sales, accurately reflect the business results and limit the risks tax settlement, at the same time enhance financial transparency and effective governance.