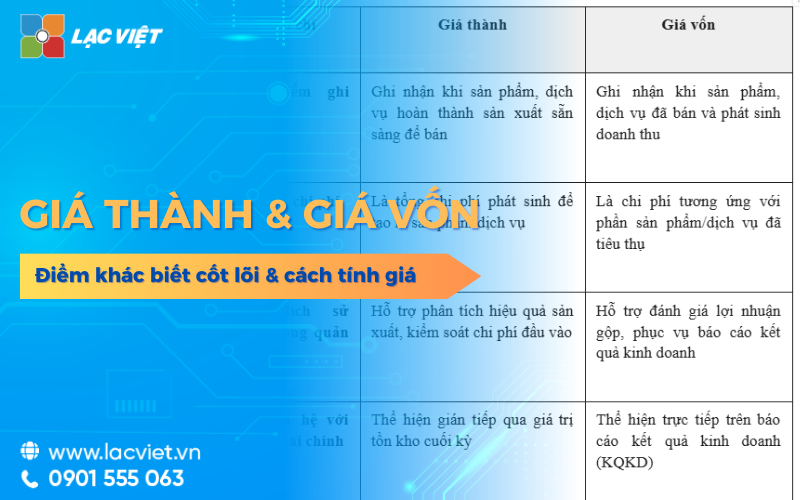

Production accounting is the accounting department track, gather and analyze all costs incurred in the manufacturing process to properly calculate the price of the product. This activity helps businesses control costs, determine the profit for decisions about price, production plans. accounting company produced just serve the financial statements, is both important tools for operation management in manufacturing enterprises.

Many businesses have difficulty when deploying business accounting, manufacturing do not define the right audience set costs, choosing the wrong target allocation formula or reviews unfinished products not in accordance with the peculiarities of production. As a consequence, the price is wrong, profits not reflect the actual accounting data do not support is for the executive producer.

The same Lac Viet learn in detail how to organize business accounting production standard: from the collection, classification, cost to the accounting of the business peculiarities, product reviews unfinished to price as well as the end states according to current regulations.

1. Accounting what is the production? Businesses are required?

1.1 accounting what is the production?

Accounting in the production department is on track – analyze costs incurred in the process of product formation, from when to put the raw materials into production until finished product. Other than accounting trade or service only focus on sale, purchase, accounting, production company, reflects the level of consumption of resources within the enterprise, through which just serves financial statements medium support cost control to governance decisions.

The role of business accounting, manufacturing, located in place:

- Determine the price of precision: to help businesses build strategic selling price in accordance with input costs actual and expected profits, room escape condition, sale, or valuation lack of competition.

- Optimized & cost effective manufacturing: provides detailed metrics to help leadership detect waste, cost analysis beyond the level, from which suggestions for improvement process production.

- Support planning, production & budgeting: accounting data is input important to plan production – cost – budget. Help balance resources, finance, operate, practical.

- Increase transparency & legal compliance: Ensure the report, the cost of compliance with accounting standards and tax rules, limiting the risk, check out later.

1.2 any Business required to organize production accounting?

The business has manufacturing operations need accounting organization to control costs, calculating the right price. If not done correctly, business to profit “virtual” as well as lack of reliable data to operate, improve production.

- Business production according to orders: Activities according to the individual requirements of each client, or the contract, with the cost structure is different for each unit. If not, the organization of accounting in each order, business quotes, inaccurate and difficult to control interest – hole.

Accounting production as orders, help set the cost right practice, decision-support receipt, control, profits, and enhance business efficiency.

- Business manufacture series: Popular in industries such as apparel, food, electronic components, construction materials, with the production characteristics of large, repeat along the chain and costs incurred repeatedly on each workshop, the production.

Production accountant role calculate the price of the average track fluctuations in cost, timely recognizes the element of profit decline, thereby supporting business control business performance overall.

- Business machining, OEM: Usually bear requires cost transparency from the partner of the contract clearly stipulates the cost structure, the level of wastage and method of settlement. In this model, the accounting is both base and settlement, protect the rights of business when the dispute arises, just to help accurately assess the efficiency gains of the contract.

- Business has multiple stages, more workshops, more necklaces: can Not just accounting costs at the company level, as this will not be sufficient basis to assess the effectiveness of each department and production stage.

In that context, production accountant needs to gather and analyze costs according to each stage, workshops and necklaces. As a basis for leadership recognition point wasting, performance evaluation and investment decision making improvement, restructuring production in a sustainable way.

For accountants business production, the organization of accounting of production requires not only compliance, which is the foundation of administration, cost-effective operation. Business as large-scale, complex process, or the high level of competition, the role of accounting becomes more and more important.

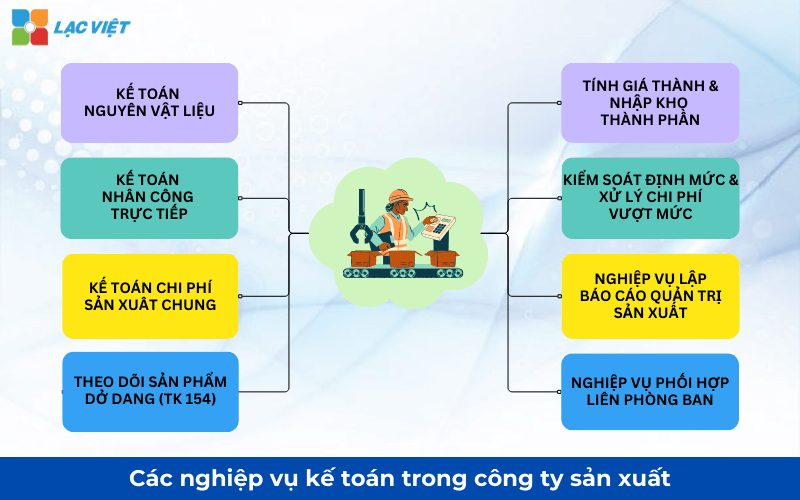

2. The task of accounting in business production

In financial management – accounting, business accounting, manufacturing not only record data, but also provide information service, cost control as well as decision-making executive. The track details the cost from raw materials to finished products help businesses optimize resources, improve the profit margin.

2.1. Track production costs

Business accounting manufacturer is responsible for tracking accounting of the types of costs incurred during the production process, including:

- Raw material directly (NVL): this is the cost of the supplies directly involved in the production of products, for example steel in mechanical fabric in apparel. Track NVL help businesses control number, as well as raw values actual consumption, thereby avoiding losses reduce inventory costs not necessary.

- Direct labour (NC): recorded salaries, allowances and other terms related to workers directly involved in production. This data is directly related to the productivity of labor is the basis to allocate costs to each product.

- Production overhead (cost efficiency general): this is the cost can not be attached directly to a specific product, such as electric water workshop, depreciation of machinery and maintenance costs. The track cost efficiency general help businesses understand the cost of manufacturing activity overall as well as the appropriate allocation on the cost of the product by the final match.

When these costs are tracked properly and timely, leaders can analyze in detail the cost of production in each group, thereby identifying the factors that cause waste, as well as offer solutions to adjust the production process for more efficiency.

2.2. Product price calculator

One of the key tasks of production accounting is to determine the price of the exact product. Price is the full cost of production was recorded on each unit of product, including NVL, NC and the allocated cost efficiency general.

Allocated indirect costs (cost efficiency general) in a logical manner are key requirements to ensure every unit products bring the right part of the cost respectively. For example, the cost of electricity production machine can be allocated according to the hours of machine operation, helping to closely reflects the actual costs incurred for each product.

Calculate the price of true help business plan price match guarantee covers the cost to reach the target profit. At the same time, the price data is also the basis for comparison with the market price – a decisive factor in pricing strategy, bid.

2.3. Warehouse management & inventory

Inventory management is an important task associated with the track line raw materials, products in the entire production cycle:

- Track input – output – inventory of raw material, semi-finished products and finished products.

- Collation of material fact at the warehouse with bookkeeping in order to timely detect deviations in import and export inventory.

- Sorting inventory by status (parked, are produced, finished).

Effective inventory management helps businesses reduce working capital is packed in inventory, avoid shortages of materials before production, reduce the cost of storage. This is especially important in the context of the cost of raw materials usually occupy a large proportion in the total cost of production.

2.4. Manage fixed assets & tools production service

Fixed assets (machinery, equipment), tool support is an essential part of manufacturing operations.

Accounting duties:

- Tracked, recorded from fixed assets when shopping to when put into use.

- Depreciation, i.e. the allocation gradually the cost of the property by using life cycle to reflect the true cost of used machinery for production.

- Management tools, small retail production service to avoid losses and ensure support tool for production.

Tracking, depreciation helps businesses properly allocate costs on the production has the benefit received. From there, ensure expense reports properly reflect the efficient use of assets.

2.5. Reporting the cost of production – prices

Business accounting production must set the type of report serves both internal administration, financial statements:

- Report production costs: reflect actual costs used in production.

- Report price: presentation of costs on each unit of product, help to assess production efficiency.

- Report analysis: compare actual costs with cost plan or norms to detect trends in cost overruns.

These reports help business leaders grasp activity and compare the results between the states or parts of production, from there take timely decisions.

2.6. Control the use of supplies & control public debt

Production accounting to control the use of raw materials according to the norms have to plan for timely detection of deviations. This has important implications in the control costs, optimize resources.

Besides, the control of public debt with customers and suppliers to ensure business idea income and expenditure fact, avoid the risk of lack of working capital or dispute with partner.

3. Principles of accounting according to the circular current

Production accountant just to adhere to the norm, just serve cost management and decision making. Currently, the business applied Information private 99/2025/TT-BTC or circular 133/2016/TT-BTC. The principles of accounting to ensure accurate data, consistent, and reflect the production efficiency.

- Expenses are recorded according to the matching principle: Into the correct states arise to reflect the true cost of production in each period. Compliance with this principle helps enterprises with accurate data, avoid accumulated cost wrong states guarantee profitable results, analysis results reflect the true fact.

- Set the cost according to subject costs: such as products, orders, workshop or production stage to clearly determine the costs incurred for each part of the manufacturing process; this classification help businesses compare the results between the object recognition where are consuming, high cost, and as a basis to adjust, improve operational efficiency.

- Allocation of indirect costs under the form of logical consistency: like hours, machine hours, or output to apply consistency between the states. To properly reflect the level of consumption of resources, avoid discrepancies in price between the products.

- Product reviews unfinished fit the peculiarities of production: unfinished products need to be evaluated according to the degree of completion actual costs were incurred. In accordance with the peculiarities of production, to reflect the correct cost as well as the business results of states, at the same time avoiding the recorded costs of early or late.

- Prices reflect actual costs incurred: both direct – indirect, as a basis for determining the selling price estimation to analyze profits; as the price reflects the true cost of the business will determine the profit margin to the fact avoid risk of selling below cost due to lack of cost control.

Adhere to the principles of accounting production not only help businesses meet the requirements of accounting standards but also create a platform reliable data to compare the cost according to the product and strategic decisions about the selling price, the optimal production activities. At the same time detect waste, improve operational efficiency.

4. Guide service accounting company manufactured according to current regulations

Business accounting, production not only in the recognition of expenses incurred, which must be held accounted for throughout the entire production cycle – cost – effective evaluation. Here are detailed instructions each group of professional with the account, the accounting standard for business can apply directly.

4.1. Professional accounting materials in production

In the business of manufacturing and materials as inputs directly accounted for a large proportion in the price and should be followed up in detail by warehouse, by lot and for the purpose of use. The classification of clear main material, filler material, fuel, packaging, as well as compare the actual use with the norm to help businesses control costs, timely detection, attrition unusual.

Accounting:

- When buying raw materials enter a warehouse:

Debt TK 152 – Raw materials

Debt TK 1331 – VAT is withheld (if available)

Have TK 111/112/331 - When raw materials directly to production:

Debt TK 621 – the Cost of raw materials directly

Have TK 152 - When the material used for the workshop:

Debt TK 627 – production Costs, general

Have TK 152

This is to help enterprises better control inventory, reduce the loss of raw materials and create the platform accurate data for the calculation of the price.

4.2. Accounting costs directly

Costs directly reflect the cost of labor directly involved in the manufacturing process products. Not only stop in the recorded salaries, production accounting longer have to allocate costs according to each product, stages or order to evaluate the effectiveness of labor.

Accountants need to combine data timekeeping, payroll, and production completed to keep track of labor cost in real time to control the expenditure exceeding the norm.

Accounting

- Recorded wage workers direct manufacture:

Debt TK 622 – Cost, direct labour

Have TK 334 – pay workers - Extract the account under payroll (SOCIAL insurance, health INSURANCE, UNEMPLOYMENT insurance, KPCĐ):

Debt TK 622

Have TK 338 – accounts payable salary

Information costs is an important basis for enterprises evaluating labor productivity, adjust the production plan accordingly.

4.3. Accounting production costs, general

Production overhead is the costs incurred in the factory, but can not be determined directly for each product, including water, electricity, depreciation of machinery, maintenance costs, cost management workshops as well as tools production service.

Due to the nature indirectly, if not held accounting and rational allocation of production costs in general, very easy to falsify the product price.

Accounting

- When production overhead incurred:

Debt TK 627 – production Costs, general

Have TK 111/112/152/214/331 - Final allocation of the cost of joint production for products:

Debt TK 154 – the Cost of production, unfinished business

Have TK 627

Selection criteria allocate suitable as hours, product quality or cost help price reflects the true level of consumption of resources of each product.

4.4. Accounting track unfinished products

Unfinished products as the product has not yet completed at the time of the end states, but has incurred the cost of production. This is a peculiar trait important in accounting manufacturing company, directly affect the cost as well as profit in each period.

The entire cost of raw materials, workers and the general production after the set are reflected on the TK 154 – the Cost of production, unfinished business.

Accounting

- The shipping cost of production in the states:

Debt TK 154

Have TK 621, 622, 627

End of the period, accounting rate value products unfinished by the method in accordance with the production process to avoid false trading results.

4.5. Accounting calculating cost of products

The calculated price is the core business of business accounting, manufacturing, reflecting the full cost spent to create finished products. Production accountant needs to identify the right audience calculate the price of such products, semi-finished products or order, at the same time choose the method of calculating the cost of matching production model.

Accounting

- When the finished product warehouse:

Debt TK 155 – Finished products

Have TK 154 – the Cost of production, unfinished business

After the accounting needs to analyze the difference between the actual cost. Plan to evaluate the effectiveness of production in order to support decision adjusting the selling price or the production process.

4.6. Accounting norms & analysis difference

Accounting according to the norms are important tools to help businesses control costs in the production process. On the basis of the raw materials as well as the workers were built, accounting compare the actual cost incurred to determine the difference.

- The cost in the norm is accounted normal to the account, 621, 622, 627.

- Case the costs exceed the norm and determined to be not reasonable, accounting, accounted for separately in order to properly reflect the efficient production:

Debt TK 632 – cost of goods sold or TK 811 – other Expenses

Have TK 621, 622, 627

The accounting, analysis difference help leaders identify causes of cost overruns and take measures to improve timely.

4.7. Business reports, manufacturing management

Management reports of production is formed directly from the system accounting, especially the account, 621, 622, 627, 154 and 155. Accounting is not recorded more pen new algorithm, but must scrutinize the normalization of data prior to reporting.

The administration report usually includes expense reports according to the product, report the performance report each workshop and report comparative plan – fact. This is a tool that helps leaders assess the effect of a given operating decisions in a timely manner.

4.8. Service coordination related departments

Each pen accounting production are derived from the data of the departments to offer. Votes import – export warehouse is base accounting of raw materials. Timesheets, payroll is base accounting costs. report output is allocation base cost as well as price.

The coordination between accounting with inventory, production, hr and technical department helps to ensure accounting of true essence, data consistency have high value to use for business management.

5. The accounting profession related & pen general accounting in business production

Group business this ensures contact information the entire cycle of production accounting from input – production – consumption – financial end – to-end states of material prices as well as business results are fully reflected, exactly.

5.1 Group of professional input

Business service inputs reflect the procurement, warehousing and used materials, tools and supplies in the production, is the basis to control costs as well as price.

| Profession | Objects / case | The account | Notes |

| Buy NVL warehousing | Buy unpaid |

|

Increased investment, increased debt |

| Payment by cash/NH |

|

Increase supplies and reduce money | |

| Buy CCDC warehousing | All forms |

|

Similar to buying NVL |

| Cumshot CCDC use | Allotted 1 times (small type) |

|

Brought straight into the cost |

| Allocate more times (large type) |

|

Wait allocation gradually | |

| Periodic allocation | Monthly/quarterly |

|

Quote from 242 to the cost |

Properly accounted professional input to help businesses control supplies right from the start limit deviations costs, prices.

5.2 Group professional output

Group business output reflects the sale of finished products, revenue recognition, the price of capital and deductions related, is the basis to determine the business results.

| Profession | Content details | The account |

| Semi-finished products / products | Revenue recognition |

|

| Recorded the price of capital | Export warehouse of finished products |

|

| Deductions | Trade discount |

|

| Sales returns |

|

|

| Re-enter the inventory return |

|

Accounting full professional head out to help businesses identify the right revenue, price of capital and profit, at the same time ensure data financial transparency.

5.3 Group business debts – finance

Group business liabilities – financial reflecting keeping track of accounts receivable and payable and cash flows related to sales activities, payment.

| Profession | Content details | The account |

| Sale bear products | Track debts and customers |

|

| Collect money, cheap debt | Customer payment |

|

| Debt comparison | End of the accounting period | For projection, balance TK 131, 331; treatment difference according to |

Good management business debt help businesses control cash flow, limiting the risk of bad debts ensure balance financial stability.

5.4 Group business end of

Group business end of the period reflects the synthesis of cost, costing, transfer revenue – cost determine the results of the business of the accounting period.

| Stage | Profession | The account (Debt/Available) |

| Production & Prices | The CP materials directly |

|

| The CP Staff directly |

|

|

| The CP general Manufacturing |

|

|

| Warehousing of finished product |

|

|

| Identify & SUMMARY | The transfer of net Sales |

|

| The shipping cost of goods sold |

|

|

| The shipping Cost of sales & QLDN |

|

|

| Final results | If the business has INTEREST |

|

| If business loss |

|

Done right business end of the period to help businesses determine the exact price, guaranteed profits, data, financial statements reflect the true state of operation.

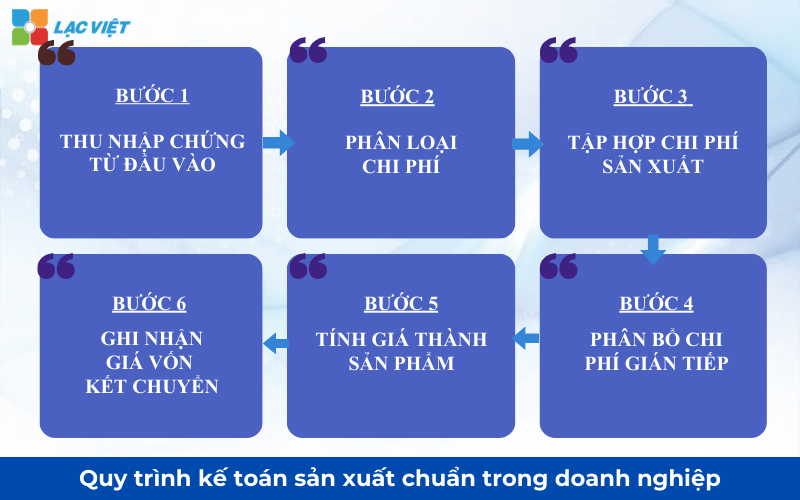

6. Process production accounting standards in the business

Accounting process, the production company is the sequence of steps profession to ensure that expenses are recorded in full, the right audience, properly and is the correct transfer into the product price. A standard procedure not only help enterprises comply with regulatory accounting – tax, but also create a data platform for cost management as well as executive producer.

Step 1: collect stock from input

Voucher is the legal basis services for the entire operation accounting. In this step, production accountant need to closely coordinate with the relevant department to collect the full stock from arising in the period, including:

- Import – export of raw materials, tools and supplies

- Timesheets, payroll, production workers

- Invoice cost of electricity, water, maintenance, depreciation of machinery

- Minutes, testing semi-finished products, finished products

Control of documents right from the start helps to reduce errors, avoid costs, or recorded not the right audience, especially in the business there are many workshops or more orders in parallel.

Step 2: classify costs according to elements & objects

After collecting evidence from accounting to conduct classification of cost according to two angles in parallel:

- According to cost elements: raw materials, direct labor, direct production costs, general.

- According to the subject costs: products, orders, stage, workshop or production line.

Sorting right from the beginning helps the set cost price in the following steps be performed quickly and accurately.

Step 3: Set the cost of production

In this step, the entire costs incurred that is integrated into the account the cost corresponding to the current regulations. The accountant should ensure:

- Raw material costs are recorded properly the actual number used for production.

- Costs are allocated according to the right time, output and labor.

- Cost of joint production is full set, do not overlook the indirect costs.

Set the full cost is a prerequisite to price properly reflect the actual production.

Step 4: allocate indirect costs

Production overhead should be allocated according to the criteria in accordance with the peculiarities of production of the enterprise, for example:

- Allocated according to the time machine for business use more machinery.

- Allocated according to the hours of labor for business-intensive workers.

- Allocated according to the production or consumption rate.

Important principles is the final allocation must be reasonable, there are base and is applied consistently between the accounting period to ensure comparability of the data.

Step 5: Calculate the price of the product

After collection, as well as cost allocation, accounting proceed to calculate the price of products by subjects was determined. Price includes the entire production costs actually incurred in the period, after adjustment unfinished products first period – end.

Results the calculated price is the basis to:

- Determine cost of goods sold

- Compare with retail price, the profit margin

- Analysis of the effect produced by each product or order

Step 6: Record the price of capital & transfer

End of the accounting period, the accounting done:

- Recorded capital price of the product has consumed

- The shipping cost of production to the price of capital in accordance with the regulations

- Collated data between cost accounting – inventory – production

The accurate reporting business results reflect the performance of the business during the period.

7. The difficulty often encountered in business accounting production

Although playing the central role in cost management, production accounting, in fact often encounter many challenges, especially in the business medium & large.

- Cost data dispersion, lack of contact information: Costs incurred from many different parts such as warehouse, manufacturing, human resources, technical. If the data is not contact information, accountants must synthetic crafts, easy occurrence of deviations and delays.

- Calculate the price of slow, inaccurate: Many businesses just calculate the price after the end of the quite long. Meanwhile, data indicative of “past statements,” no more value to the decision-making executive in a timely manner.

- Much depends on Excel: using Excel discrete in management costs, the price of potential risks such as: wrong formula, duplicate data and difficult to control versions. Especially when the production scale expanding, Excel no longer meet the requirements management details of the multi-dimensional easy to falsify information to serve the decision.

- Difficult to control the level & the difference: If there is no tracking system norms and real comparison – planning, business difficult to detect causes of cost overruns, leading to waste, you can not be handled promptly.

The difficulty on not derived from the accounting profession that from way to organize data as well as administrative tools. When the information was scattered, and handling and a lack of contact information, accounting, manufacturing companies can not provide timely data, for reliable operating. This reduces the admin role of accounting limited the ability to control the cost of business.

8. Accnet ERP – Solution management accounting for business production

AccNet ERP is management solution overall is designed in accordance with special production enterprise in Vietnam, meets at the same time requires accounting – tax as well as the needs of internal governance. The system allows businesses to control the entire value chain of production, from raw material input to price as well as efficient product output.

Specific AccNet ERP support for business:

- Materials management closely the multi-dimensional: in the warehouse, by lot, according to stage and follow orders, help control inventory, reduce the loss, as well as the optimal working capital.

- Automatically set & allocation of production costs: the cost of raw materials, labor costs, overall production was recorded. Allocated according to the criteria flexibility, in accordance with the characteristics each model produced.

- Calculate the price of fast, accurate: the price is calculated according to each product, orders, or workshops to help businesses capture timely, efficient production instead of only data after the end of the period.

- Contact information of data between the department: accounting – inventory – production – personnel be connected on a single system, eliminating the status of data dispersion, duplicate and false.

- Provide reporting systems administrator, multi-dimensional report: cost reports, price analysis report variances plan – fact, help leadership make decisions based on real-time data.

INTEGRATED AI ACCELERATION CONVERTER OF ACCOUNTING

AI in AccNet ERP't just stop at automate data entry, but also:

- Identification & classification certificate from smart: AI scan, read & sort invoice, voucher, receipt, limit errors due to input manually.

- Financial forecasting & budget: the system uses algorithms machine learning to forecast cost, revenue, business support decision fast.

- Warning risk accounting: AI to detect abnormalities in the book, from which timely warning of false or fraud risks.

- Reports assistant smart: AI suggested report template, automatic data aggregation support, leadership, financial analysis instant.

BUSINESS IS WHAT WHEN IMPLEMENTING ACCOUNTING SOFTWARE LAC VIET?

- Experience more than 30 years develop software solutions business management in Vietnam.

- Ecosystem of comprehensive: AccNet ERP easily connect with other solutions of Lac Viet (HRM, Workflow, Portal...).

- Advanced technology: Integrated AI support, cloud & on-premise flexible.

- Services dedicated support: A team of knowledgeable professionals with accounting – finance in Vietnam, companion throughout the deployment.

- Trust from thousands of customers in many areas: finance, banking, manufacturing, trade, services.

Production accounting not only to comply with accounting standards, but also is the foundation data for cost management, operating businesses. The accounting set cost allocation, it reflects honest, efficient production, profit. When the accounting system is designed to operate consistently and businesses better control resources and costs. Since then, leaders have the basis of reliability to detect waste, as well as improve operational efficiency.

![[ĐẦY ĐỦ] Mẫu báo cáo tài chính, tình hình tài chính file excel theo Thông tư 200 và 133](https://lacviet.vn/wp-content/uploads/2025/04/mau-bao-cao-tai-chinh.png)

![[Trọn bộ] File Excel mẫu báo cáo chi phí sản xuất kèm hướng dẫn lập chi tiết](https://lacviet.vn/wp-content/uploads/2025/02/bao-cao-chi-phi-san-xuat.png)