Accounting cash advance orders for the seller's business accounting is done when business advance part of the payment for supplier before receiving enough goods or services, the Debit account, 331 (to be paid To seller) & Have account 112 (bank deposits). This helps to manage the public debt, tight, ensure transparency of costs, at the same time accurately reflect the situation of the property with the obligation in the financial statements.

However, in practice many businesses still have difficulty in the implementation of the correct accounting standards lead to errors in the profession. Therefore, mastering prescribed the same method of accounting cash advance goods under circular no. 200/2014/TT-BTC & circular 133/2016/TT-BTC not only help businesses comply with the law on accounting standards but also enhance the effective management of public debt, optimize cash flow to support planning, more accurate billing.

The same Lac Viet find out details about the profession, principles recorded and the process advances to customers standards in business.

1. Cash advance bank what is? Why do I need accounting?

Advance money order is a payment that businesses make to the supplier prior to receipt of goods or services. This is a form of popular trades in the financial management business, especially when businesses want to ensure the rights of purchase, priority orders, or take advantage of the deals from vendors such as early payment discount.

The advance money to the seller not only a financial manipulation merely, but also reflects the ability to manage cash flow, risk management in the efficient operation of business.

Through this, businesses can balance between demand, production, business as well as financial possibilities out there, build sustainable relationships with suppliers.

The role of accounting cash advance orders for the seller:

- Ensure a stable supply of: cash advance helps business to be the preferred supplier order fulfillment, restrictions, shortages of raw materials, avoiding production interruptions or slow the progress of business, especially in the peak period.

- Cash flow management efficiency: accounting cash advance purchase helps business proactive allocation of money to plan a reasonable payment. This not only reduce the pressure paid irregularly but also help enterprises take advantage of discounts for early payment, optimize operational costs.

- Support debt management – risk control: accounting cash advance purchase helps business proactive resource allocation money and planning reasonable payment, reduce the pressure paid irregularly, at the same time take advantage of the discount early payment to the optimal cost of operation.

- Increased transparency – decision support purchase: recognition and management closely the account of advance help leaders fully embrace spending information, from which a decision to purchase the right time and to negotiate conditions more effectively with suppliers.

- Create advantages in relations with suppliers: Business done in advance is usually a priority of delivery or receipt of the terms of trade facilitation. This helps to optimize the supply chain, enhance competitiveness in the market.

2. Rules of accounting cash advance purchases for the seller

Accounting cash advance item to the seller is clearly stated in the circular 200/2014/TT-BTC and circular 133/2016/TT-BTC. The implementation of regulations and help ensure the bookkeeping accurate time improve the efficiency of debt management and cash flow of the business.

2.1. Circular no. 200/2014/TT-BTC & circular 133/2016/TT-BTC

Two circular on the given detailed instructions on the recorded track to collate the advance to suppliers. A number of core content includes:

- Instructions recorded professional advance – payment – debt: When a business cash advance goods to the seller, the accountant should recognized immediately at the time of the transaction, does not depend on whether the goods received or not, to accurately reflect the liabilities and closely monitor the status of the transactions with suppliers.

- Use accounts accounting as specified: circular, 200 & circular 133 are specified

- Account 131 – pay the seller be used to reflect the amount of business the rest of the money to pay as well as payment obligation reality with suppliers.

- Account 111 – Cash & account 112 – bank deposits used to record the amount of business was spent to advance.

- Rules of evidence from the cross–: circular require businesses to have more votes, credential details, contract of sale, or agreement to advance to bases of accounting.

In addition, the business must make for projector periodically between the department of accounting – purchase – inventory to ensure accurate data between goods received amount did not advance.

2.2. Accounting principles related

Besides adhere strictly to account, business to perform accounting for advance money to the seller according to the accounting principles prescribed in the circular 200/133:

- Recorded when incurred the obligation of payment: advance must be recorded at the time of business transfer money to the supplier, does not depend on the time of receipt of goods, to reflect the true financial situation and liabilities at each time point.

- Contrast – adjust when receiving goods: When receiving the goods or services, accountants record the goods, raw materials, or expense, respectively, at the same time the transfer did not advance to reduce the debt provider. If advance amount greater than the value of goods receipt, keep track of the balance in advance; on the contrary, if the value of a larger amount did not advance, noting the difference is the debt to pay additional.

- When handling returns or cancellation of contract: the case of returns or cancellation of orders:

- Businesses have to adjust reduce the balance of advance was recorded.

- Recorded funds are supplier refunded or deducted from the purchases below.

The adjustment must have full stock from: the minutes cancel orders, receipts, pay orders, invoices adjusted,...

3. Instructions on how accounting advance the money to the supplier in accordance

Accounting for advance money for the goods to the offer should be made in the correct sequence, service and guarantee fully reflect the flow of money spent, the value of goods received and the liabilities fact.

Here are detailed instructions for each case accounting common as well as comply with the accounting standards under circular no. 200/2014/TT-BTC & circular 133/2016/TT-BTC.

3.1. Accounting accounting as cash advance to suppliers

When businesses need to advance a portion or the entire amount of the recorded pens payment must be made carefully based on the base stock from full to ensure accuracy and transparency. The evidence from basic include: payment receipt or credential details, contract of sale, the proposal, the approval of the leadership and the other relevant documentation.

Accounting notes, business accounting, cash advance for goods to the seller is done as follows:

- Debt TK 131 – pay seller: Reflects the amount of business has advance to suppliers. The Debit TK 131 help accounting accurately track each account, the unknown number of payments made, amount to pay, at the same time classified according to each vendor to easily manage public debt.

- Have TK 111 – Cash (if paying by cash) or TK 112 – bank deposits (if transfer): Reflects the actual amount of business was spent. The credited TK 111/112 ensure cash flow management transparency, help businesses control the exact amount of money pulled out of the fund or a bank account.

For example, suppose company A purchases raw material from supplier B with a contract worth $ 200,000,000, business agreed to advance 50% of the value of the contract by bank transfer.

Accounting entries when the advance will be:

- Debt TK 131 – pay seller: 100,000,000

- Have TK 112 – bank deposits: 100,000,000

Explanation:

- The amount of 100 million was recorded on TK 131 shown obligations business has to pay in advance for supplier B.

- TK 112 credited reflect the actual amount was deducted from your bank account for payment, guaranteed cash flow out is accurately reflected.

When receiving, the accounting will be recorded value of raw materials, warehousing and for minus the amount of advance on TK 131. Helps to balance public debt with suppliers always right, avoid mistakes and to support cash flow management efficiency.

3.2. Accounting accounting on delivery – payment of the debt

When goods or services have been suppliers handover, the accountant should be noted increase in assets or expenses, respectively. At the same time, the money did not advance will be for except on TK 131.

Case 1: value of using the right amount of advance

- Debt TK 156/152/155 (the purchase Price of goods, raw materials, finished products)

- Have TK 131 – paying the seller

After accounting for this, the balance of TK 131 at supplier will be about 0.

For example: Business A advance 100 million for vendor B. When goods receipt, the value of the right 100 million:

- Debt TK 156 – finished goods: 100,000,000

- Have TK 131 – pay seller: 100,000,000

Case 2: value larger amount of advance

Businesses also have to pay more:

- Debt TK 156/152/155

- Have TK 131 (value advance)

- Have TK 111/112 (part longer have to pay extra)

For example: Business A advance 100 million, but when you received the goods, the actual value is 150 million:

- Debt TK 156 – cargo: 150,000,000

- Have TK 131 – 100,000,000

- Have TK 112 – 50,000,000 (the rest payment)

Case 3: value smaller amount did not advance

- The remainder of the front rest is the track on TK 131, not recorded at cost or inventory.

- Account this will be deducted the next time you shop or wait for provider reimbursement.

For example: Business A advance 100 million but the value of the fact only 80 million:

- Debt TK 156 – cargo: vnd 80,000,000 dong

- Have TK 131 – vnd 80,000,000 dong

- The first 20 million is still on track TK 131, for except on the next purchase.

3.3. Debt comparison with providers

Work for lighting public debt is an important step in financial management for business, to ensure data between the enterprise and supplier always match up exactly. This is especially important when there is the account of advance, because deviations in recorded public debt can lead to payment status scraps, missing or duplicate, affect financial statements cash flow business.

The steps taken for debt comparison:

Step 1: Check balances TK 131 according to each supplier:

- General accounting all accounts, accounting for advance money to the seller, to pay debt and payments made to each provider.

- Clearly define balance beginning of the period, arisen in the states as well as the closing balance.

Step 2: collate between contracts, invoices, enter – voucher advance:

- Compare the value of goods and services received with the amount that has been advanced.

- Check the legal documents enclosed as contract of sale, voucher, credential details, receipt of goods.

- Timely detection of flaws as noted, teen, payments or errors in advance.

Step 3: Confirm the debt periodically with supplier:

- Recurring monthly or quarterly, send the aggregate liabilities to the supplier for confirmation.

- Set the minutes for projectors signed confirmation from both parties.

- Recorded every adjustment of public debt arises, ensure data dovetail with reality.

Debt comparison often helps to detect errors on time, reducing financial risks as well as enhance transparency in the management of public debt. At the same time, each time adjusting the balance advance to be accompanied by legal documents in full to ensure accountability and storage service, audit or internal reporting.

For example: company A has a balance of TK 131 with supplier B is 100 million (advance), extra 50 million in January. When the projector:

- Accounting verified suppliers have delivered the goods worth $ 140 million, VAT invoice in full.

- The balance of the front left is 10 million, is on track TK 131 to subtract on the next purchase.

- Memorandum for projector is set up and confirmed between the two sides, ensure transparency avoid a dispute about the debt.

3.4. Case accounted for returns or order cancellations

In the purchase process, there may occur situations such as: supplier non-delivery and lack, delivery of wrong, or changing business needs lead to cancellation of the contract. Meanwhile, the accountant must perform the step adjustment of balance advance on TK 131 to ensure public debt reflects the true reality.

The processing steps:

- Adjust the reducing balance TK 131:

- Accounting determine the advance related to the order being returned or cancel the contract.

- This amount will be reduced directly on TK 131, ensure public debt with supplier reflect accurate.

- Supplier refund:

- When a provider return the funds did not advance, accounting recorded an increase of cash or bank deposits:

- Debt TK 111/112 – Cash/bank deposit

- Have TK 131 – paying the seller

- The recognition of this ensures cash flow to the fact is fully reflected in the financial statements.

- When a provider return the funds did not advance, accounting recorded an increase of cash or bank deposits:

- Account advance is retained to except into other contracts:

- If the supplier retains advance to deductions for the next purchase, accounting continue to monitor the balance on TK 131 as usual.

- Updated information on the management system, public debt in order to avoid confusion when paying the contract after.

Note: Any adjustment of advance must have full legal documents such as minutes of paid orders, invoices, adjustments, or the contract cancelled, at the same time get timely updates on the accounting system and public debt. Business need for screening and confirmation of balances with suppliers after each adjustment to ensure accuracy, consistency and transparency.

For example: company A has the first 50 million for supplier B, but then business decision to cancel the contract due to changes in demand:

- Supplier repay the entire advance:

- Debt TK 112 – bank deposits: 50,000,000

- Have TK 131 – pay seller: 50,000,000

- Balance TK 131 to 0, ensure public debt factual.

In case, the supplier retains 20 million to minus on other contracts:

- TK 131 still recorded 20 million, according to a deduction when executing the next transaction.

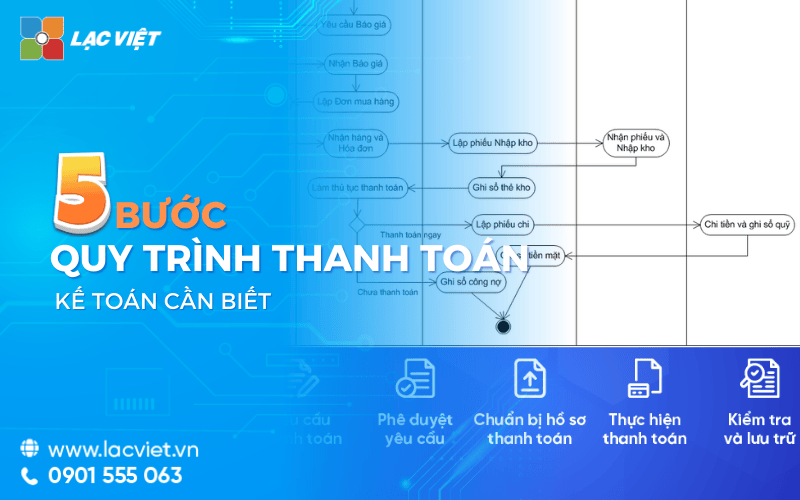

4. Process accounting for advance money to the seller

Process accounting for advance money to the seller should be coordinated between the purchasing department, accounting and warehouse to ensure accuracy, transparency and compliance with accounting standards. Below is the standard procedure applied in business:

Step 1: Confirm the request in advance – collate purchase contract

- Purchase parts set suggestions in advance based on the basis of the contract of sale, quotation or agreement, deposit with the offer. In this proposal, purchase department should specify the details includes the required amount of the advance, the rate of advance in comparison with the total value of the contract, the expected time to receive the goods, the payment conditions, aims to use goods or services.

- Accounting then conduct a thorough inspection of the payment terms, the rate of advance delivery time as well as the related conditions in the contract, at the same time collated with other relevant documents such as coupons, cost, quote, memorandum of agreement on deposit, to ensure the advance is valid, accurate and in accordance with the budget as well as shopping plans of the business.

- After full inspection, business leaders approved the proposal in advance according to internal processes, confirm that the payment is legitimate, in accordance with the actual needs within the range of the budget is approved.

This step helps enterprises limited risk details wrong, avoid advance money to the seller not true demand or no legal basis, while ensuring the management, cash flow, debts and to create transparency and coordination between the purchasing department, accounting as well as leaders in the monitor/control the advance.

Step 2: Set up payment receipt/authorization chi – profile advance

After the proposal prior application is approved, payment accounting, conduct of payment receipt if payment by cash or the debit authorization if payment via bank transfer. Payment receipt/authorization details must accurately reflect the amount of advance, provider name, billing purposes, as well as information related to the contract of sale to ensure transparency easily check and compare later.

Record the advance should be the full set, including:

- Recommended before had been purchasing department as well as leadership approval.

- The contract of sale between the enterprise and supplier, specify the clear value, the number of the same conditions of delivery.

- Quotes or orders to compare the value, the guaranteed payments right with the agreement.

- Decision on approval of the leader, confirmed the account of advance legal at the same time fit the budget.

- Payment receipt/authorization details are then chief accountant & director-approved according to the level of responsibility, to create the legal basis sufficient to ensure internal control.

Full set records not only create legal grounds firmly to pen the student but also ensure compliance with processes, internal control, which helps businesses manage cash flow efficiently, track debt tightly to minimize the risks of errors or disputes with suppliers.

Step 3: Recorded in accounting books according to the correct account specified (TK 131/111/112)

After payment vouchers as payment receipt, or authorized expenditure is approved in full, accountants conduct recorded in advance on the ledger. Journal entries recorded to be carried out as follows:

- Debt TK 131 – pay the seller: Recorded amount of business has advance payment to suppliers, expressed payment obligations remaining under the contract of sale.

- Have TK 111 – Cash / Có TK 112 – bank deposits: Reflects the cash flows fact have the funds or transfer from your bank account, ensure financial statements properly reflect the cash flow of the business.

As prescribed in circular no. 200/2014/TT-BTC & circular 133/2016/TT-BTC, the time recorded entry this is right when account accounting cash advance to the seller that arise, do not wait until the goods are delivered. This ensures the data on the ledger is always accurate, fully reflects the payment obligations under the cash flow of the business at each time point.

Step 4: track – for projectors – make payment on delivery

When goods or services are delivered parts warehouse establishment receipt and receipt to confirm quantity, quality as well as the actual status of the goods. This is the basis for the accounting purchase order to receipt – bills – contracts – evidence from the advance to ensure all information is properly matched with the actual transaction.

After the screening, liabilities accounting made journal entries to transfer the before record the receipt of goods about:

- Debt TK 156/152/155 – value goods and raw materials or the finished product (depending on the type of goods receipt)

- Have TK 131 – paying the seller – The advance was used for payment.

To handle the difference between the value of goods & advance:

- Teen advance: If value of goods greater account was, the accountant recorded the rest to additional payment on TK 111/112.

- Brunette advance: If value of goods less than the advance, the advance remains on track TK 131 to deducted the next time you shop or wait for provider reimbursement.

Then, conduct business debt comparison periodically with suppliers to ensure the entire transaction dovetail with reality.

6. The important note in accounting money

To account for advance money to the seller efficiency, ensure accuracy and compliance with accounting standards, companies should note the following points:

- Risk control cash flow – accounting errors: Made recorded the account of advance correctly, in the correct amount and time of birth. Periodically check the journal entries to avoid omission, mistake, or advance beyond the affordability of the business.

- Store stock from full transparency: Each transaction in advance to be accompanied by invoice, payment receipt, contract of sale or agreement. The full archive help businesses easily collated, auditing and accountability when necessary.

- Collated periodically between accounting, warehouse – room purchase: make The comparison of data between departments to ensure the data about cash advance items match the actual inventory, orders, and public debt. This helps in the timely detection of deviations, ensure transparency and accuracy in the administration.

- Compliance with legal regulations – accounting standards: accounting advance to follow the circular no. 200/2014/TT-BTC or circular 133/2016/TT-BTC, avoid mistakes in financial statements and tax settlement.

- Decentralization – internal control: assign clear responsibility for approval in advance, as well as recorded journal entries, limiting the risk of fraud, or to use money for improper purposes.

7. Accounting software Accnet – optimal Solution of the accounting profession for Vietnamese enterprises.

Software Accnet ERP helps businesses effectively manage the advance money, reduce risk and improve the efficiency of financial management:

- Automatic record advance – payment: All transactions in advance is the system recorded automatically, minimize errors due to input manually, ensure the accuracy and timeliness.

- Track public debt according to the supplier: the System for projection, balance, automatic warning when exceeding the limit of public debt help debt management stricter and more transparent.

- Detailed reports, accurate: LV-DX Accounting provides the synthesis report as well as detailed analysis of advance, debt and cash flow, support the accounting department with purchase smart decisions.

- Compliance with accounting standards – legal: Help businesses implement accounting advance in accordance circular no. 200/2014/TT-BTC and circular 133/2016/TT-BTC, ensure financial reporting transparency and accurate.

INTEGRATED AI ACCELERATION CONVERTER OF ACCOUNTING

AI in AccNet ERP't just stop at automate data entry, but also:

- Identification & classification certificate from smart: AI scan, read & sort invoice, voucher, receipt, limit errors due to input manually.

- Financial forecasting & budget: the system uses algorithms machine learning to forecast cost, revenue, business support decision fast.

- Warning risk accounting: AI to detect abnormalities in the book, from which timely warning of false or fraud risks.

- Reports assistant smart: AI suggested report template, automatic data aggregation support, leadership, financial analysis instant.

BUSINESS IS WHAT WHEN IMPLEMENTING ACCOUNTING SOFTWARE LAC VIET?

- Experience more than 30 years develop software solutions business management in Vietnam.

- Ecosystem of comprehensive: AccNet ERP easily connect with other solutions of Lac Viet (HRM, Workflow, Portal...).

- Advanced technology: Integrated AI support, cloud & on-premise flexible.

- Services dedicated support: A team of knowledgeable professionals with accounting – finance in Vietnam, companion throughout the deployment.

- Trust from thousands of customers in many areas: finance, banking, manufacturing, trade, services.

The use of Accnet ERP not only optimize the process of accounting for advance money to the seller but also improve the efficiency of financial management, create a solid foundation for the buying decision as well as manage public debt smart.

Accounting for advance money to the seller in accordance with regulations to help businesses control public debt, tight, optimize cash flow and ensure transparency in financial reporting. When done properly process from recorded, collated to the processing arise, businesses can minimize the risk of errors, and active in the procurement plan at the same time improve the efficiency of management. A standardized processes not only help comply with legal but also create advantages in working with suppliers and business support, stable operation, durable.

![[ĐẦY ĐỦ] Mẫu báo cáo tài chính, tình hình tài chính file excel theo Thông tư 200 và 133](https://lacviet.vn/wp-content/uploads/2025/04/mau-bao-cao-tai-chinh.png)

![[Trọn bộ] File Excel mẫu báo cáo chi phí sản xuất kèm hướng dẫn lập chi tiết](https://lacviet.vn/wp-content/uploads/2025/02/bao-cao-chi-phi-san-xuat.png)